All Categories

Featured

Table of Contents

Keep in mind, however, that this does not say anything about readjusting for rising cost of living. On the bonus side, also if you presume your option would certainly be to purchase the supply market for those 7 years, and that you would certainly get a 10 percent yearly return (which is much from specific, particularly in the coming decade), this $8208 a year would certainly be greater than 4 percent of the resulting nominal supply worth.

Instance of a single-premium deferred annuity (with a 25-year deferral), with four payment options. The month-to-month payout here is highest for the "joint-life-only" alternative, at $1258 (164 percent greater than with the prompt annuity).

The way you get the annuity will certainly determine the answer to that question. If you purchase an annuity with pre-tax bucks, your costs decreases your taxed revenue for that year. According to , getting an annuity inside a Roth plan results in tax-free settlements.

What does a basic Secure Annuities plan include?

The advisor's very first step was to create a thorough economic plan for you, and after that describe (a) exactly how the suggested annuity suits your overall strategy, (b) what alternatives s/he thought about, and (c) just how such alternatives would certainly or would not have actually led to lower or greater compensation for the expert, and (d) why the annuity is the remarkable option for you. - Fixed-term annuities

Naturally, an expert may try pushing annuities even if they're not the very best suitable for your scenario and objectives. The factor could be as benign as it is the only product they market, so they drop victim to the proverbial, "If all you have in your tool kit is a hammer, rather soon everything begins resembling a nail." While the advisor in this scenario might not be unethical, it increases the danger that an annuity is a poor option for you.

Annuity Investment

Given that annuities typically pay the representative selling them a lot greater compensations than what s/he would certainly receive for investing your cash in mutual funds - Deferred annuities, not to mention the zero payments s/he 'd receive if you purchase no-load common funds, there is a big incentive for agents to push annuities, and the much more complex the better ()

A dishonest expert recommends rolling that amount right into new "much better" funds that just happen to carry a 4 percent sales load. Agree to this, and the advisor pockets $20,000 of your $500,000, and the funds aren't likely to carry out much better (unless you chose even a lot more poorly to start with). In the same example, the advisor could guide you to purchase a challenging annuity with that $500,000, one that pays him or her an 8 percent commission.

The advisor tries to hurry your decision, claiming the deal will certainly quickly disappear. It may certainly, yet there will likely be comparable deals later. The advisor hasn't figured out exactly how annuity settlements will be taxed. The expert hasn't revealed his/her settlement and/or the fees you'll be charged and/or hasn't revealed you the influence of those on your ultimate repayments, and/or the compensation and/or fees are unacceptably high.

Current rate of interest rates, and hence predicted payments, are traditionally reduced. Even if an annuity is best for you, do your due persistance in contrasting annuities offered by brokers vs. no-load ones sold by the providing firm.

How do I get started with an Annuity Contracts?

The stream of regular monthly repayments from Social Safety is comparable to those of a deferred annuity. Since annuities are volunteer, the individuals getting them typically self-select as having a longer-than-average life span.

Social Security benefits are totally indexed to the CPI, while annuities either have no rising cost of living protection or at many supply an established percent yearly boost that may or may not make up for inflation completely. This type of motorcyclist, similar to anything else that boosts the insurance firm's risk, requires you to pay more for the annuity, or accept reduced repayments.

Immediate Annuities

Please note: This write-up is meant for educational objectives only, and must not be considered financial recommendations. You ought to seek advice from an economic expert prior to making any significant economic choices.

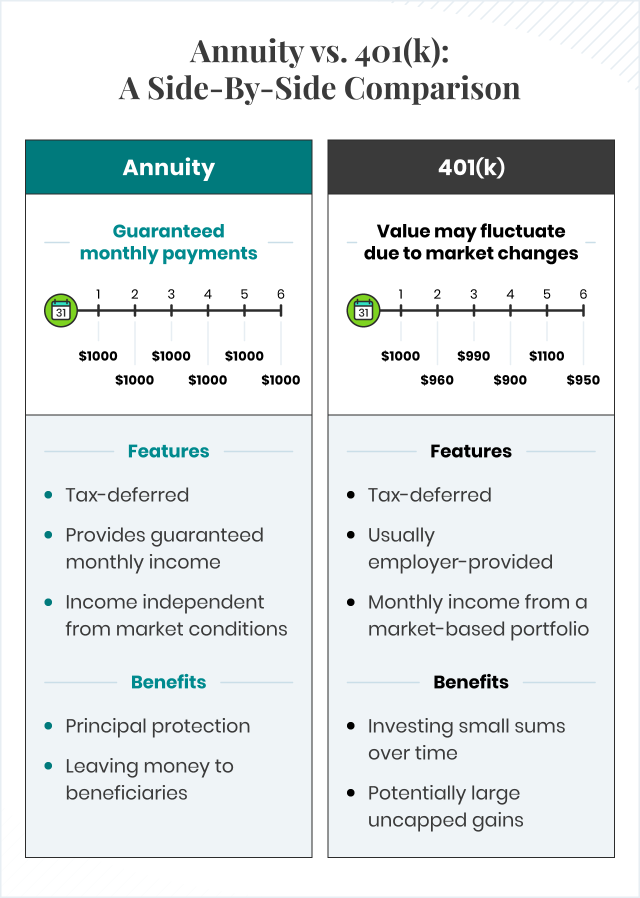

Because annuities are planned for retired life, tax obligations and charges may apply. Principal Protection of Fixed Annuities. Never shed principal as a result of market performance as taken care of annuities are not bought the market. Also throughout market downturns, your money will not be impacted and you will certainly not shed money. Diverse Investment Options.

Immediate annuities. Made use of by those who desire dependable earnings promptly (or within one year of acquisition). With it, you can customize revenue to fit your demands and produce earnings that lasts for life. Deferred annuities: For those who wish to grow their cash with time, however agree to postpone access to the cash up until retired life years.

Who should consider buying an Annuity Investment?

Variable annuities: Offers better possibility for growth by investing your cash in financial investment options you choose and the ability to rebalance your profile based upon your choices and in a manner that aligns with altering monetary goals. With taken care of annuities, the business invests the funds and provides a rate of interest to the customer.

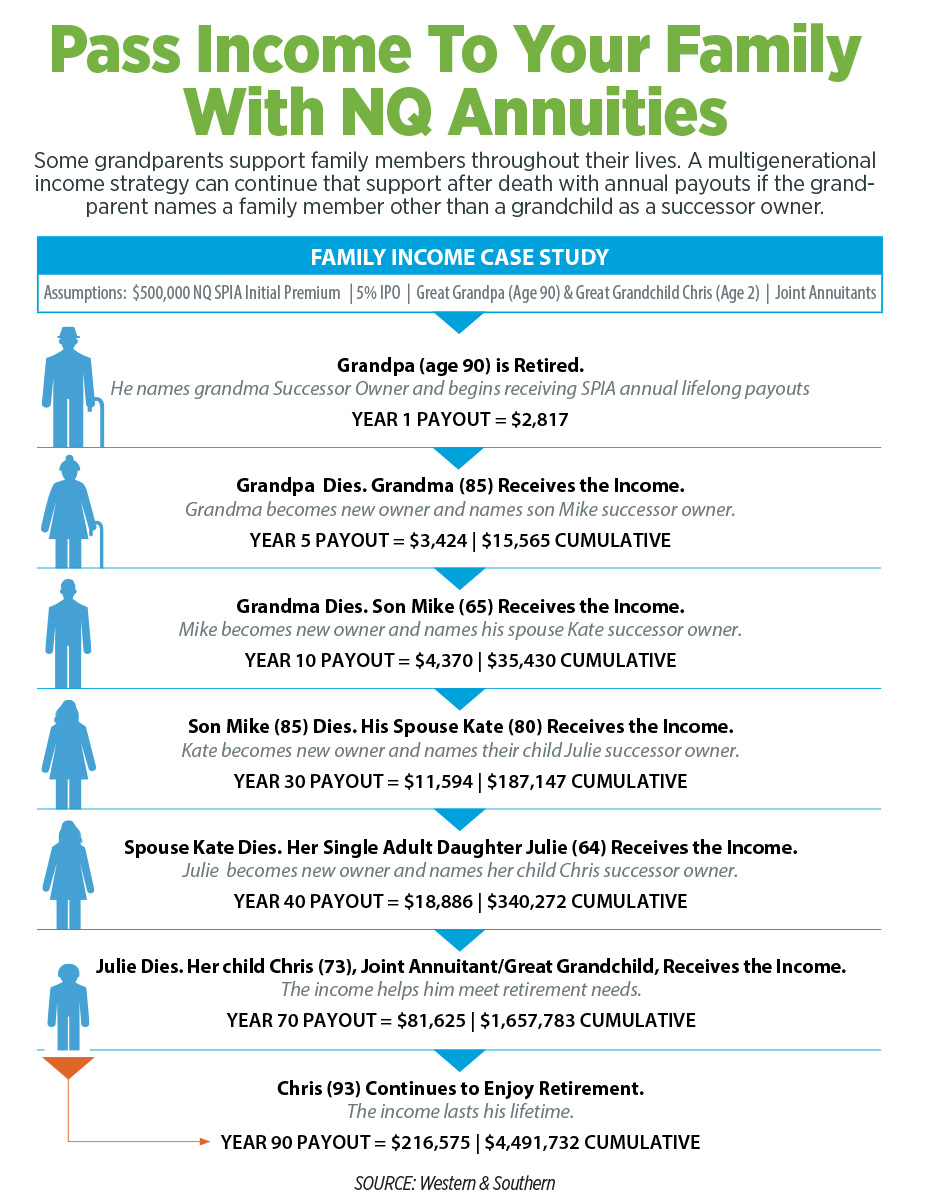

When a death insurance claim accompanies an annuity, it is vital to have actually a named recipient in the contract. Different choices exist for annuity death advantages, depending upon the contract and insurance company. Selecting a refund or "duration certain" option in your annuity provides a death advantage if you die early.

Why is an Long-term Care Annuities important for my financial security?

Naming a recipient other than the estate can help this process go much more smoothly, and can help make certain that the profits go to whoever the private desired the money to go to rather than going via probate. When present, a death advantage is immediately included with your contract.

{kind=link}

Table of Contents

Latest Posts

Analyzing Strategic Retirement Planning Key Insights on Annuities Variable Vs Fixed Defining the Right Financial Strategy Benefits of Choosing the Right Financial Plan Why Fixed Income Annuity Vs Vari

Breaking Down Pros And Cons Of Fixed Annuity And Variable Annuity Key Insights on Your Financial Future Breaking Down the Basics of Choosing Between Fixed Annuity And Variable Annuity Benefits of Choo

Breaking Down Fixed Vs Variable Annuity Pros Cons Everything You Need to Know About Financial Strategies Breaking Down the Basics of Variable Annuity Vs Fixed Annuity Pros and Cons of Various Financia

More

Latest Posts